For all the drama surrounding Biden’s latest Strategic Petroleum Reserve fiasco and his admin’s ridiculous idea to “stimulate” US energy producers to pump more oil because, you see, Biden promises to buy oil at some unknown point in the future (he may or may not, but right now he is certainly draining a million barrels of emergency US energy lifeblood just to buy a few midterm votes, assuring energy producers have zero incentive to produce more), the real crisis is not oil or gas, but diesel.

The problem is that as we repeatedly warned over the summer, even as others were transfixed by the moves in gas, see:

… the crisis gripping the US diesel market is getting out of hand, as demand is surging while supplies remain at the lowest seasonal level for this time of year ever, according to government data released Wednesday.

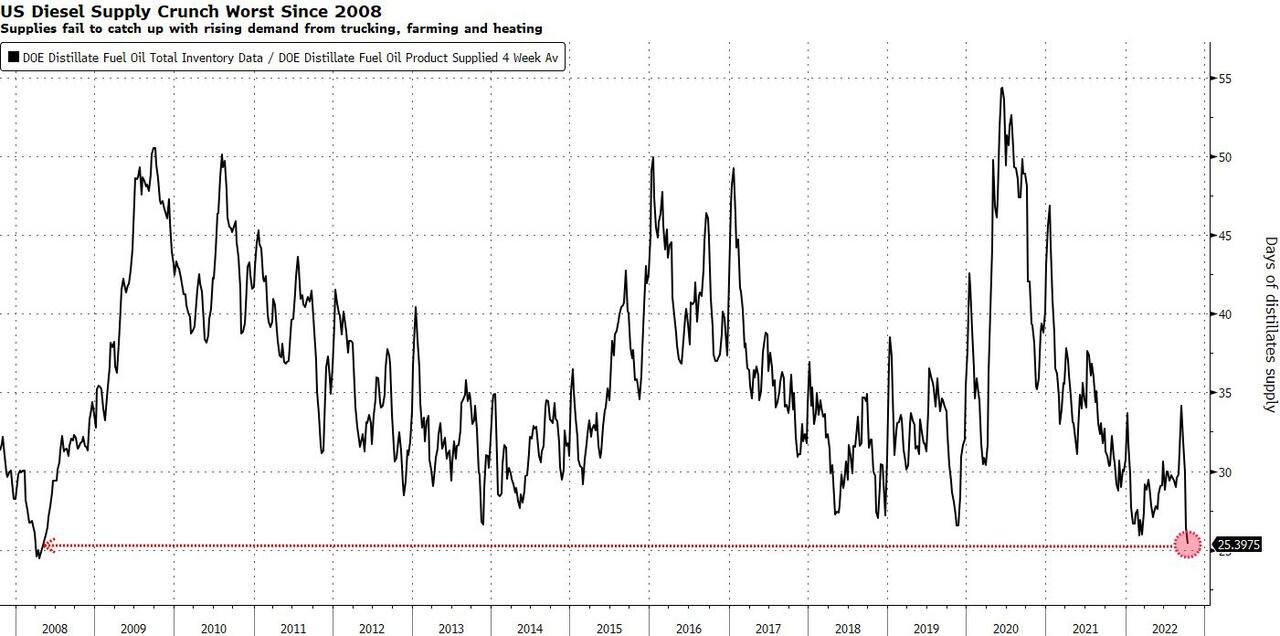

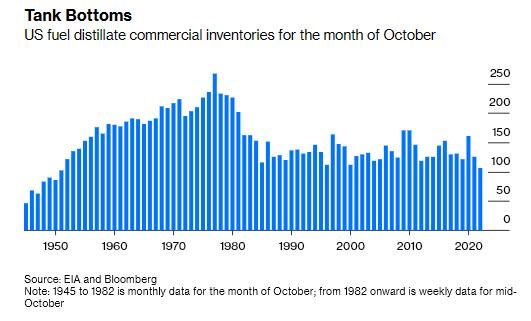

According to the EIA, the US now has just 25 days of diesel supply, the lowest since 2008; and while inventories are record low, the four-week rolling average of distillates supplied – a proxy for demand – rose to its highest seasonal level since 2007.

In short, record low supply (courtesy of stifling regulations that have led to a historic shortage of refining capacity) meet record high demand. What comes next is, well, ugly (while weekly demand dipped slightly in the latest week, it’s still at highest point in two years amid higher trucking, farming and heating use).

The shortage of the fuel used for heating and trucking and – generally speaking – to keep commerce and freight running, has become a key worry for the Biden administration heading into winter, perhaps even bigger than the price of gas heading into the midterms (well, not really). As Bloomberg’s Javier Blas writes, “such low levels are alarming because diesel is the workhorse of the global economy. It powers trucks and vans, excavators, freight trains and ships. A shortage would mean higher costs for everything from trucking to farming to construction.”

National Economic Council Director Brian Deese told Bloomberg TV Wednesday that that diesel inventories are “unacceptably low” and “all options are on the table” to build supplies and reduce retail prices.

But while the White House claims to be so very concerned about the coming diesel crisis, it is doing absolutely nothing besides draining the SPR which has zero impact on diesel production.

The historic diesel crunch comes just weeks ahead of the midterm elections and will almost certainly drive up prices for consumers who already view inflation and the economy as a top voting issue. Retail prices have been steadily climbing for more than two weeks. At $5.324 a gallon, they’re 50% higher than this time last year, according to AAA data.

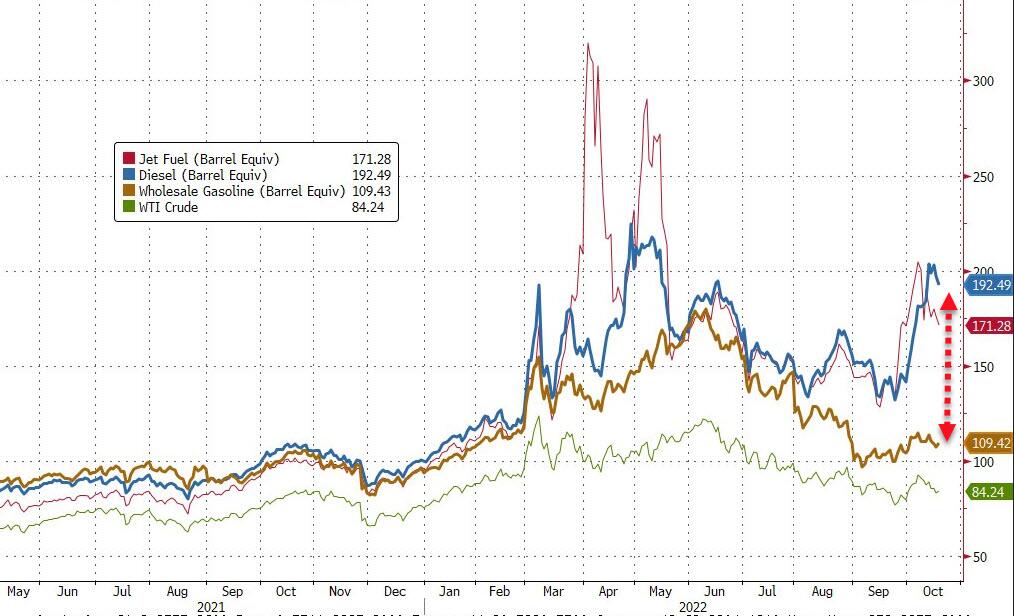

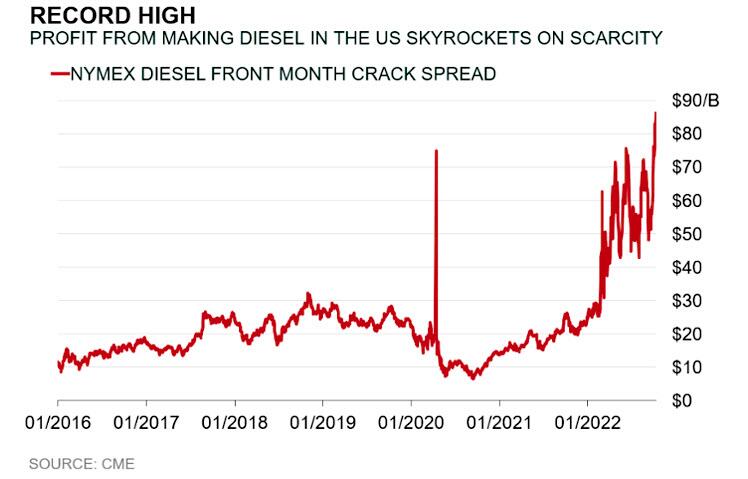

Wholesale diesel prices in the spot market of New York harbor, a key pricing point, have surged this week to more than $200 per barrel. Excluding a brief interval from late April into mid-May, that would be a record high.

As a result, American refiners are enjoying the best-ever diesel margins, with the profit of turning a barrel of crude into one of diesel – i.e., the diesel crack spread – hitting a record high of $86.5 per barrel, up roughly 450% from the 2000-2020 average of $15.7 per barrel.

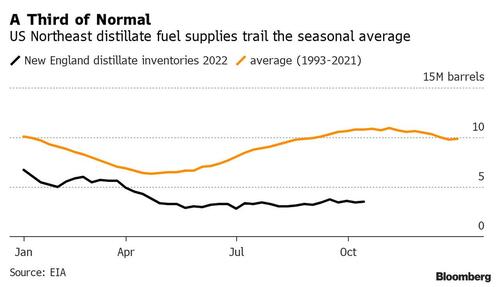

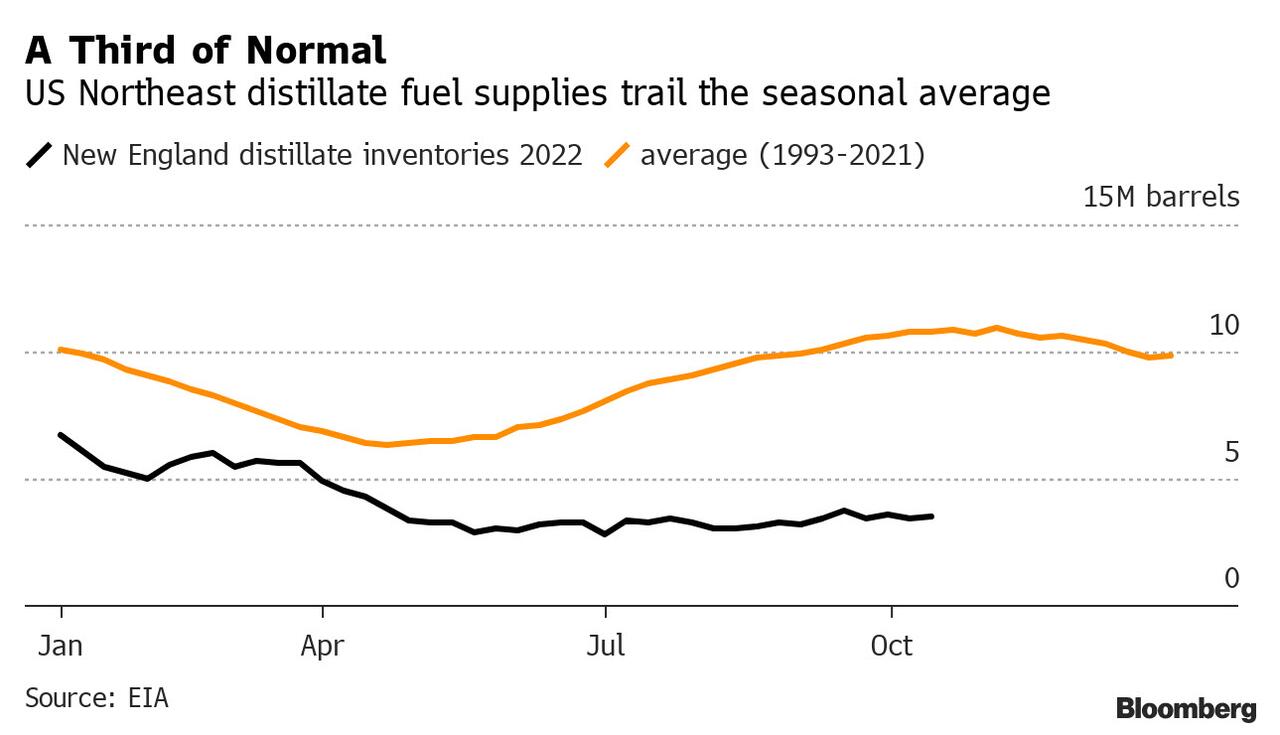

This isn’t all that surprising. as we have been warning all year, the American diesel market has been in crisis mode for most of 2022; if only others had caught on this crisis may have been averted. But now, it’s too late, and national stockpiles have drained as refiners entered maintenance season and as Russia’s war in Ukraine tightened global supplies and limited imports. Meanwhile, market backwardation – where prompt deliveries are priced at a premium over future deliveries – has made building inventory extremely costly, feeding into a vicious cycle of tight supplies and price spikes. In New England, where more people burn fuel for heating than anywhere else in the country, stockpiles are less than a third of typical levels for this time of year.

The reasons for the collapse in inventories and the price surge are four-fold.

- First, local diesel demand has recovered quicker than gasoline and jet-fuel from the impact of the pandemic, draining stocks.

- Second, foreign demand is also strong, with American diesel exports running at unusually high level.

- Third, and according to many, most important of all, the US also has lower refining capacity than before, reducing its capacity to make fuels.

- Fourth is Russia’s invasion of Ukraine. The US was importing a significant amount of Russian fuel oil before the war, which its Gulf of Mexico-based refiners turned into diesel. The trade ended after the White House sanctioned Russian petroleum exports.

Some relief is on the way, courtesy of those handful of international sources of commodities that the Biden admin hasn’t declared an implicit war on. At least two vessels carrying around 1 million barrels of diesel are due to arrive in New York after being diverted from their original destinations in Europe. Delta’s Trainer refinery in Pennsylvania is also returning from seasonal maintenance, which will increase regional diesel production.

But the impact of such band aids will be tiny. As Bloomberg’s Blas writes, “the diesel crisis leaves the Biden administration facing very difficult choices. If he leaves the market alone, prices are likely to rise further before they drop; if he intervenes, either setting up minimum inventory levels or restricting exports, price increases will likely be felt elsewhere into the world. Either route will have big implications for inflation at home and for energy security in Latin America and Europe.“

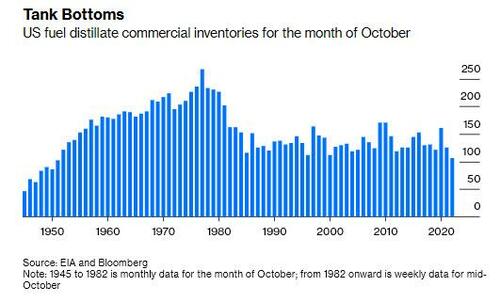

In a testament to just how clueless the Biden admin is, last spring wholesale diesel prices surged to all-time high as inventories plunged in April and May, pushing retail prices to a record high. At the time, this website (and many others) warned that we have to take urgent steps now to avoid a crisis… and nobody moved a finger; jaw bones on the other hand never stopped. Well, fast forward to now when a new crisis is in the making. America typically uses the low-demand seasons of spring and summer to rebuild its stocks of distillate fuels ahead of the winter. But it failed to do so this year – something even Europe avoided by stockpiling nat gas knowing it faces a freezing winter otherwise – and stocks are now nearly as low as they were in April, at the end of the last heating season.

If inventories decline between October and April by their 20-year average of about 25 million barrels, the US will emerge from winter with a little more than 80 million barrels in stock. That, according to Blas, is an unlikely scenario, however: The oil market would try to keep inventories from falling that much, with prices rising high enough to slow the economy, curtailing demand. Over the last 40 years, American diesel inventories have never dropped below 85 million barrels, even at the end of the heating season.

So now that the genie is out the bottle, here are the choices the Biden admin faces, all of them unpalatable:

- The White House can let the market continue doing its job, with surging prices likely denting consumption and boosting supply. With refineries enjoying sky-high margins, more diesel should be coming. But the cost of the laissez-faire approach is higher inflation and a much faster recession as US industries shut down. Because diesel increases trucking costs, it’s a particularly pernicious sort of inflation as it quickly embeds into everything that needs to be transported, lifting core inflation measures.

- If the White House opts to intervene, the less harmful measure would be to release a small reserve of diesel that the government keeps for emergencies (clearly they have no problem doing that). The Northeast Home Heating Oil Reserve only has one million barrels, so it would be, at best, a Band-Aid. But it’s better than nothing, and Biden should order its release. For those asking, releasing more crude from the Strategic Petroleum Reserve would do little to resolve the problem, since the bottleneck is refining.

- Other interventions would have significant consequences, potentially harming American allies. In Washington, officials are mulling restricting, or even banning, diesel exports. If the measure is approved, it would leave neighbors including Mexico, Brazil and Chile short of diesel. In July, the last month with available full data, US diesel exports to Latin America hit a record high of 1.2 million barrels, double the amount a decade ago.

- Another option is forcing oil companies to build up stocks quickly ahead of the winter by setting a minimum inventory level, similar to what the European Union did for natural gas stockpiles. US officials are particularly worried about the northern part of the US East Coast, where inventories are low both seasonally and in absolute terms. The region, known in the industry’s jargon as PADD1A, is where the greatest demand is: Of the roughly 5.3 million households that use heating oil in America, more than 80% are in the Northeast. The problem with a mandatory minimum stock level is that it would force American refiners to import more or reduce their exports — or both. The impact in Latin America would be noticeable. Prices in the US may decline, but they will soar elsewhere.

The bottom line, as the Bloomberg energy strategist notes, is that “the timing of today’s diesel crisis couldn’t be worse.” That’s because the EU, which relies still on Russian diesel exports, will ban imports from February onward (assuming it survives the winter). Europe will be short of diesel then, and Biden needs to consider that too. Ultimately, the imminent arrival of the bone-crushing recession will rebalance the market, reducing demand, particularly as the housing market cools and construction slows down, and consumer demand for goods declines, reducing trucking needs.

That’s a heavy price to pay to resolve the problem, but with an administration as hopelessly clueless as this one, which today blasted the following tweet to make a point yet proved just the opposite…

It’s simple: When the cost of oil comes down, we should see the price at the pump come down as well. That’s how it should work.

— President Biden (@POTUS) October 19, 2022

But right now, refiners and retailers are making record profits at the expense of the vast majority of Americans. It’s unacceptable. pic.twitter.com/h3xiyEYEdv

–

CHECK OUT THIS EPISODE OF THE TROY SMITH SHOW!

SHARE AND SPREAD THE WORD, BIG TECH IS CENSORING US LIKE NEVER BEFORE!

THE TRUTH IS AT LAUNCH LIBERTY!

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}